COVID-19: six imperatives for banks in Europe - McKinsey

With the impact of COVID-19 revolutionising the way organisations around the world operate, we look at McKinsey’s six imperatives for banks in Europe.

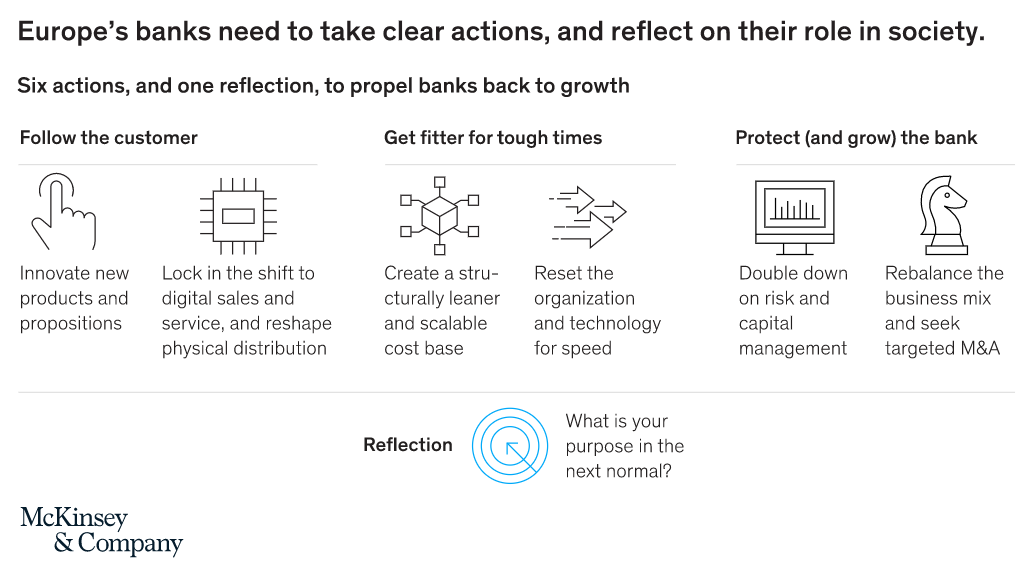

Follow the customer

1. Innovate new products and propositions

McKinsey highlights that COVID-19 has triggered a wide range of new financial needs that are waiting to be addressed. such as liquidity, retirement savings and mortgages. “Banks need to strengthen their advanced analytics skills to identify which customers they can feasibly serve and then create a personalised offer for them,” comments McKinsey, who stresses that “innovation cannot just be incremental […] Europe is home to about four thousand fintechs that have incubated disruptive propositions. Many will come under stress in the wake of the crisis—VC funding to the European fintech sector already dropped by 30 percent in the first quarter this year. Incumbent banks could acquire these innovative concepts and scale them rapidly.”

2 Shift to digital sales and service, and reshape physical distribution

“In just a couple of months, customers’ adoption of digital banking has leapt forward by a couple of years. Our most recent customer survey showed a 10 to 20 percent rise in digital banking use across Europe in April,” states McKinsey. “Such a jump in adoption opens the door for banks to turn digital channels into real sales channels, not just convenient self-service tools.”

However, the flip side to this surge has resulted in a reduction in branch capacity by roughly 20 to 30%. “Learning from this experience, banks need to redesign their physical footprint, which means rethinking the role of branches and introducing new formats.”

Get fitter for tough times

3. Create a cost base that is structurally leaner and scalable

“To offset the effect of spiking risk costs and sluggish income, and to free up resources for building digital capabilities, banks need to aim for a cost improvement of 25 to 35%, says McKinsey.

“Given the uncertainty, costs not only need to go down but also become more scalable. Banks need to find ways to move from fixed costs to pay-as-you-go models across the board, from IT infrastructure, to enterprise functions, or workspace.”

4. Reset the organisation and technology

Following the lockdown, many organisations became agile overnight - delivering ‘the impossible’.

“Banks need to lock in this speed and empower their employees by resetting their organisation from a siloed setup to one oriented around what customers value, with clear links to P&L responsibility. This means merging business with operations and IT, enabling them to react to external shifts much faster.”

Protect (and grow) the bank

5. Risk and capital management

“Credit losses will be the defining differentiator of performance over the next year, so inevitably the topic dominates board discussions across many banks,” says McKinsey, who places importance on early detection and proactive intervention to manage non-performing loans.

“Once this is under control, the next challenge will be steering through the coming recapitalisation wave.”

6. Rebalance the business mix and seek targeted M&A deals

Following a crisis industry landscapes are often redrawn. In McKinsey’s Global Banking Annual Review 2019, the company highlighted that more than half of banks already had a ROE lower than their cost of equity.

“As the pressure on ROE builds, banks need to respond by carving out non core assets that drive complexity or cost—or that simply add no value.”

To read more about the six imperatives for banks in Europe, click here!

SEE ALSO:

-

COVID-19: eight safe & successful relaunch actions - McKinsey

-

Read the latest edition of Business Chief EMEA edition, here

For more information on business topics in Europe, Middle East and Africa please take a look at the latest edition of Business Chief EMEA.